At some point in our lives, many of us will need to take out a mortgage to buy a home. Unfortunately, if you have bad credit, securing a mortgage can be challenging. Lenders are often hesitant to lend money to borrowers with bad credit because they see them as risky investments. Tribal Loans available Now. Apply directly online and get an instant decision in under 90 seconds.

However, having bad credit doesn’t necessarily mean you can’t get a mortgage. In this article, we will discuss the options and strategies available to borrowers with bad credit who are looking to secure a mortgage.

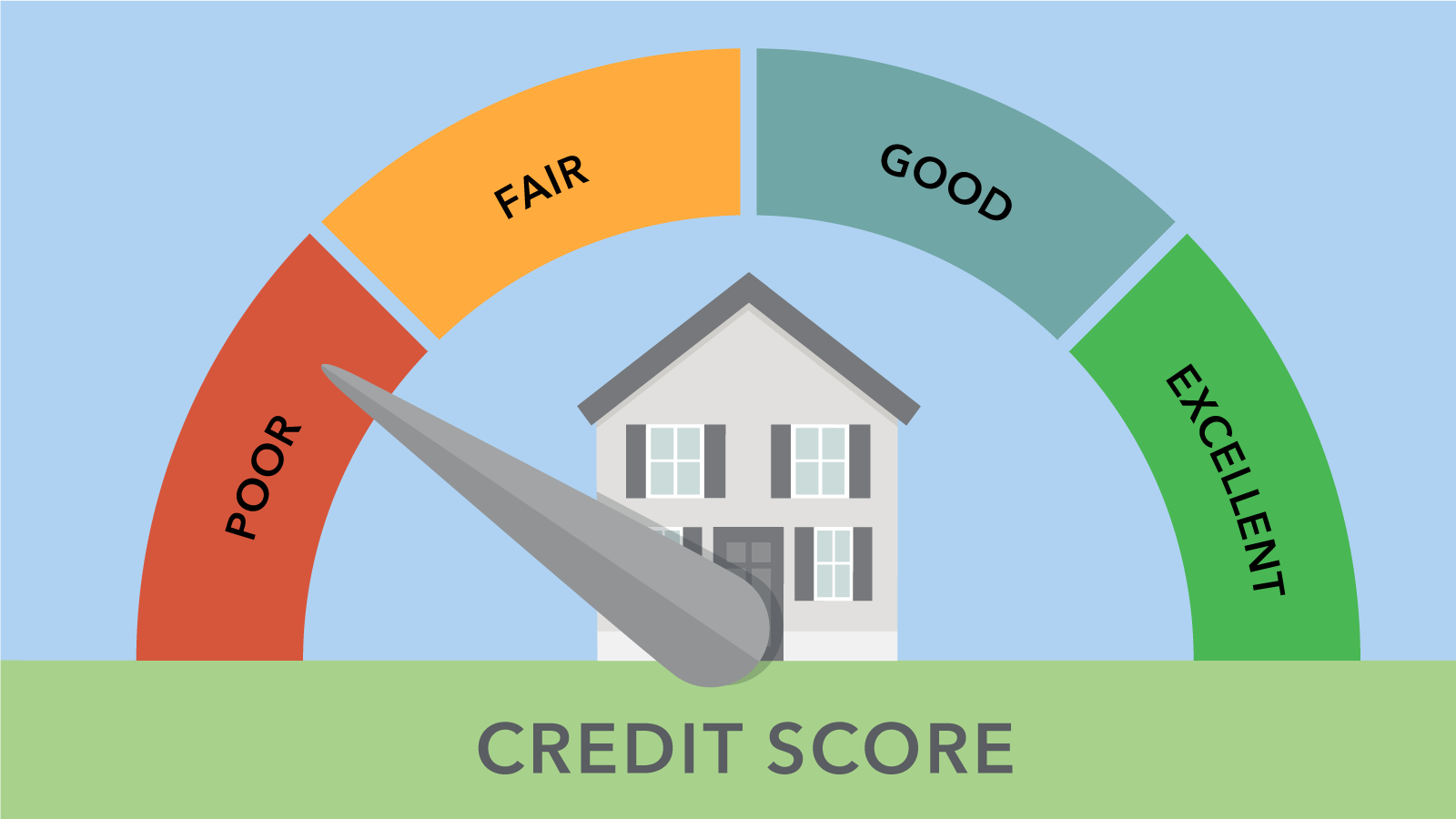

Understanding Your Credit Score

Before we dive into the options available to borrowers with bad credit, it’s important to understand what credit score is and how it’s calculated. Your credit score is a numerical representation of your creditworthiness, which is based on your credit history. Credit scores range from 300 to 850, with higher scores indicating better creditworthiness.

Credit scores are calculated based on several factors, including payment history, amounts owed, length of credit history, new credit, and types of credit used. Lenders use your credit score to determine your creditworthiness and the likelihood of you repaying your debt.

Options for Borrowers with Bad Credit

If you have bad credit, your options for getting a mortgage may be limited. However, there are still several options available to you.

FHA Loans

The Federal Housing Administration (FHA) provides loans to borrowers with bad credit. FHA loans have lower credit score requirements and more lenient credit guidelines than conventional loans. With an FHA loan, you can have a credit score as low as 500 and still qualify for a mortgage.

VA Loans

If you are a veteran or active-duty service member, you may be eligible for a VA loan. VA loans are provided by the Department of Veterans Affairs and have more lenient credit guidelines than conventional loans. With a VA loan, you can have a credit score as low as 580 and still qualify for a mortgage.

USDA Loans

The United States Department of Agriculture (USDA) provides loans to borrowers with bad credit who are looking to buy a home in a rural area. USDA loans have lower credit score requirements and more lenient credit guidelines than conventional loans. With a USDA loan, you can have a credit score as low as 640 and still qualify for a mortgage.

Subprime Loans

Subprime loans are mortgages designed for borrowers with bad credit. These loans have higher interest rates and fees than conventional loans but may be an option if you have been unable to qualify for other types of loans. However, it’s important to carefully consider the terms and fees associated with subprime loans before taking one out.

Improving Your Credit Score

While the above options may be available to borrowers with bad credit, improving your credit score can increase your chances of getting approved for a conventional mortgage with better terms and rates.

There are several things you can do to improve your credit score, including:

- Paying your bills on time – Late payments can negatively impact your credit score, so it’s important to make sure you pay your bills on time.

- Paying down debt – The amount of debt you owe affects your credit score, so paying down your debt can improve your credit score.

- Checking your credit report – You are entitled to one free credit report per year from each of the three major credit bureaus (Equifax, Experian, and TransUnion). Checking your credit report can help you identify errors and take steps to correct them.

- Avoiding opening new credit accounts – Opening too many new credit accounts can negatively impact your credit score, so it’s best to avoid opening new accounts unless necessary.